Chat with us

, powered by

LiveChat

LOGIN

Info Terkini:

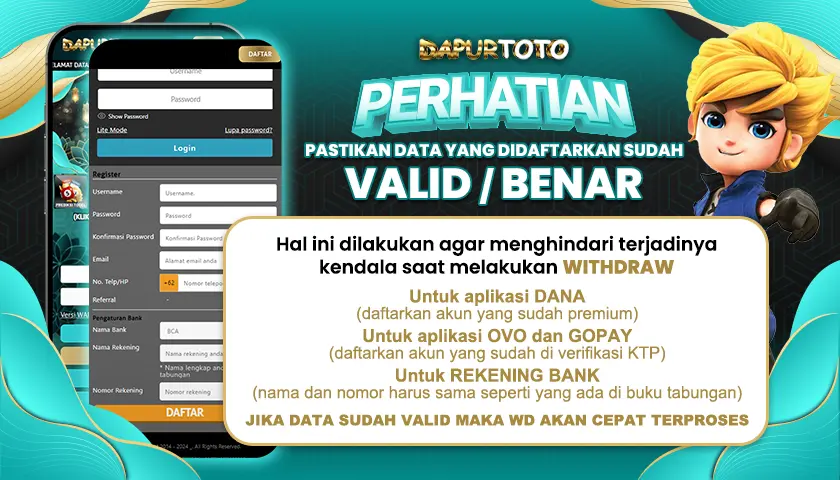

SELAMAT DATANG DI DAPURTOTO! DAFTAR SEKARANG DAN NIKMATI BETTING HANYA DENGAN 100 RUPIAH SAJA.

Cara Bermain

History Nomor

Buku Mimpi

Referral

Hubungi Kami

Lupa Password

Promosi

Daftar

Hasil Terakhir

Berita Terakhir

JADWAL TOGEL DAPURTOTO

24-03-2024 17:01:26

FAQ DAPURTOTO

01-03-2024 23:30:01

JADWAL BANK OFFLINE

01-03-2024 23:29:58

Jadwal

Bank

Bank Online (

) /

Bank Gangguan (

) /

Bank Offline (

)